9 out of 10 Homes In Kenya Own A Mobile Phone, 3 Out Of 4 Use Mobile Money

The year 2007 marked a paradigm shift in the way of doing business in Kenya. This was the year that saw one of the first mobile money payment services in the world; M-Pesa be introduced in the Kenya. Ever since, the use of mobile money payment services has become quite so common; that virtually everyone has embraced it, from the typical day laborer to the granny living in some remote village in the rural areas.

The average Kenyan use mobile money services to pay the electricity bill, groceries, water bills and now doctors too are accepting M-Pesa payment for their services. Mobile money is breathing new life into micro businesses. Companies that have adopted business models accepting mobile money payment have demonstrated that targeting some of the world’s poorest market can not only be rewarding but also a way to grow a business.

These small digital transactions (mobile money payments) are nurturing new ventures ranging from insurance companies, financial institutions, social entrepreneurship, and e-commerce among others. It is also redirecting the attention of well-established companies to a market segment that had for long been ignored; the ‘bottom billion’ or the global poor.

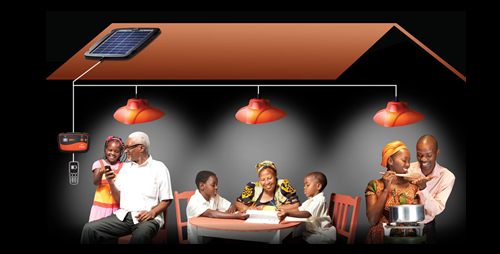

Up to November 2014, Rokoine Tipanoi, (a wife to a cow herder in Kahara Village, Kenya) had never switched on the lights in her home; never mind that she is only 52-years-old. But all that changed thanks to her mobile phone. Tipanoi uses her mobile phone to make mobile money payment in the form of small down payment to a solar panel installed on her roof that now lights her home at night.

The installment is so small that it cost the Tipanoi family less money compared to the amount they used to spend on kerosene for the lamp that used to light their home at night. They now also don’t have to make do with the smoke that came from the kerosene lamp.

The Tipanoi family is one of the hundreds of other poor Kenyan homes living either off-grid or simply can’t afford to have electricity installed in their homes. Through mobile money payments, a Kenyan social enterprise startup dubbed M-Kopa. The startup was able to bring solar products profitably to a market segment considered poor and still be able to run a successful business; one light bulb at a time.

Mrs. Tipanoi said, “Now I have two lights, instead of one lamp. And I can charge my phone.”

{kind=link}

The Tipanoi family obtained the new solar panel for a down payment of $30 and a daily installment payment of about $0.44 (Ksh.40). This social entrepreneurship venture would not have had such a smooth run, were it not for the existence mobile money in Kenya.

“The mobile phone made the bottom of the pyramid viable as a business. If you’re taking a dollar off a million people, that’s a reasonable revenue stream, but it wasn’t possible to do that without the mobile phone,” says, Aly Khan Satchu, running an investment firm in Kenya.

Kopo Kopo, another social enterprise founded by two Americans, is in the business of selling a product that enables informal retailers to accept digital payments as well as computerize their bookkeeping.

M-Changa, a Kenyan-American venture gives extended families a mobile phone app that enables them to raise money for activities like weddings and funerals. This kind of thing draws a lot of support from local communities members from all walks of life in Kenya.

Kenya’s UAP Group Insurance Company gives small farmers insurance covers and compensates them in the event their crops fail. The insurer uses satellite weather data and sometimes predicts crops failure and wires the money through mobile money to the farmers covered for crop failure risk.

The informal sector has particularly embraced mobile money payment. Users simply load their phones with cash by giving agents stationed at shopping centers, grocery stores and petrol stations. They then get a text message confirming their balance, and then they can start sending money to other people or pay for utility bills, goods, and services. They don’t need to have a bank account.

Africa in general has a growing middle class; estimated to be around 350-million. The middle class is increasingly becoming the focus of many multinationals operating on the continent. However, the poor are not featuring as much in a lot of corporate boardroom discussions, largely because they simply can’t afford most of the products on offer. They also live in areas with poor roads and infrastructures making them harder to reach out to.

Nonetheless, Africa has become a key testing ground for many micro business models. It is estimated that up to 70% of the world’s poor live in Africa. World Bank also estimates that sub-Saharan Africa had a gross national income of $1,657 per capita by 2013; largely fueled by mobile phone usage.

As at Dec. 2013, 65% of sub-Saharan Africa households had at least one mobile phone; the region also holds the title for the fastest growing mobile technology market in the world, according to Gallup data. Although most of these mobile phones are not smartphones, rather are feature phones that users load with a few dollars at a time for making calls and sending text messages. The very poor often use just text messaging services since they are comparatively cheaper.

For multinational companies targeting Africa’s most price-sensitive market, Kenya has become the suitable launching pad. Given the wide-spread use of M-Pesa mobile money.

{kind=link}

Jesse Moore, a Canadian, who is also a co-founder of M-Kopa pictured above, saw an opportunity to grow from just payments to financing the acquisition of solar panels by the poor. This social enterprise venture proved to be profitable when carried out on a mobile money payment structure. Stats show that about 35-million Kenyans live off grid and depend on kerosene lamps to light their homes at night and car batteries to charge their mobile phones.

Moore first came to Kenya, to help out in the launching of M-Pesa for East Africa telecom giant, Safaricom. He later came back to Kenya in 2012 and founded M-Kopa with two other business partners hoping that the mobile payment system will open up new opportunities.

“We believed there would be businesses built on the back of mobile payments and we wanted to be part of that,” Moore said.

The partners designed a secure system that linked the solar panels to prepaid meters. Moore admits that the hardest part was in convincing the consumers who couldn’t even afford a slight price increase in the basic goods like milk. Convincing to buy a solar panel proved quite a challenge, but the trick was in explaining to them that it could be cheaply obtained. In comparison to their expenditure on kerosene lamps, recharging their mobile phones on car batteries and a way to avoid smoke from kerosene lamps.

M-Kopa deployed their sales agents to some of the poorest regions in the country as they were very determined to tap into the most neglected market segment. Jackson Lekanayia, one of the sales agent in an area about one-hour drive from Nairobi that includes Kahara village says, in some instances, even the refundable deposit of $30 was too expensive.

“Sometimes they say they don’t have the money right now, so I give them a flier. Usually, they call back in a few weeks or a month, and they have the money,” Lekanayia said.

“Mrs. Tipanoi, who in November saw electric light inside her home for the first time, found the money for the down payment through sales of beaded necklaces. She could never afford torch batteries – much less a solar panel – but when she saw a sample a solar panel setup from M-Kopa during a weekly trip to a nearby market town, she arranged for the small daily payments.”

It would take an M-Kopa customer about a year with daily payment in order to pay off the 8-watt panel. For the Tipanois, there is now enough light to cook comfortably at night and for the two teenage children in the family to read at night without the discomfort brought about by the kerosene lamp.